Soitec reports full year ’17 results

- Solid growth in revenues: +4% at constant exchange rates

- Substantial improvement in operating profitability: current operating income up 24% to € 28m and Electronics EBITDA margin at 16.7% of sales

- Net result in positive territory: € 8m

- Net cash generated by continuing operating activities reached € 39m, up from €20m in FY’16

- Equity restored to € 149m, strong cash position of € 109m and net debt significantly reduced to € 12m

- Solid business base in RF-SOI and Power-SOI

- Further important milestones reached in the adoption of the FD-SOI technology

- FY’18 outlook: around 25% revenue growth at constant exchange rates and Electronics EBITDA1 margin2 at minimum 20%

Bernin (Grenoble), France, June 14th, 2017 – Soitec (Euronext Paris), a world leader in generating and manufacturing revolutionary semiconductor materials, today announced its full-year audited[3] results for the fiscal year 2017 (period ended on March 31st, 2017). The financial statements were approved by the Board of directors during its meeting held today.

Paul Boudre, Soitec’s CEO and Chairman of the Board, commented: “From the successful strengthening of our balance sheet through to the delivery of a strong operating and financial performance, our fiscal year 2017 has laid the foundations for a steep recovery, paving the way for higher and more profitable growth in the coming quarters. For fiscal year 2018, we expect around 25% revenue growth at constant exchange rates whilst our Electronics EBITDA margin should stand at a minimum of 20%.

Our confidence in these prospects is based on the relevance of our advanced semiconductor materials to meet the needs of the consumer electronics markets for greater performance, lower power consumption, higher reliability and optimized costs. Whether for automotive or industrial applications, for Internet of things or wearables, for smartphones or data centers, our innovative substrates and processes enable electronic systems to create value for everyday life.

The adoption of the FD-SOI technology by the semiconductor industry is gaining momentum. A few FD-SOI technology-based products have now been released for automotive and Internet of things applications. Our decision to go ahead with investing in capacity dedicated to FD-SOI wafers at our French industrial site in Bernin is fostered by further commitments made by strategic clients to build FD-SOI capacity and extend the FD-SOI roadmap,” added Paul Boudre.

Solid revenue growth and substantial improvement in operating profitability

As previously reported, Soitec’s refocus on Electronics operations decided in January 2015 was virtually completed on March 31, 2016. Consequently, the FY’17 residual income and expenses related to Solar and Other activities are reported under ‘Net result from discontinued operations’, below the ‘Operating income’ line, meaning that down to the line ‘Net result after tax from continuing operations’, the Group consolidated income fully and exclusively reflects the Electronics activity as well as the Group’s corporate functions expenses. The FY’16 financial statements have been restated to ensure comparability with the FY’17 financial statements.

Group consolidated income statement (part 1)

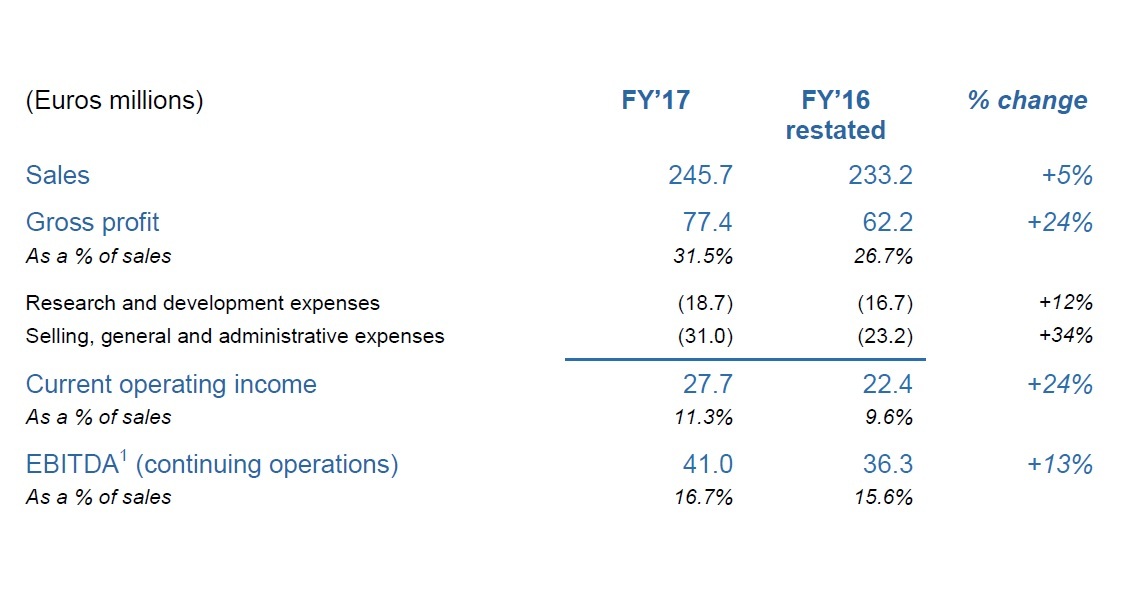

Consolidated FY’17 revenues came to 245.7 million Euros, a 5% increase (+4% at constant exchange rates), compared with the previous financial year.

- This growth was driven by higher sales of 200mm wafers (74% of sales) which rose by 6% at constant exchange rates, supported by the steady demand for radio frequency and power electronics applications in the mobile and automotive markets.

- Sales of 300mm wafers (23% of sales) also recorded positive growth (up 5% at constant exchange rates) despite the anticipated decline of the PD-SOI product line. This growth came from the other 300mm products, i.e. FD-SOI, RF 300mm and new Emerging SOI products.

- Revenues from royalties and IP (3% of sales) went down by 29% at constant exchange rates compared to the exceptionally high level recorded last year.

Gross profit reached 77.4 million Euros (or 31.5% of revenues) in FY’17, up from 62.2 million Euros (or 26.7% of revenues) in the previous financial year. This is essentially due to the new product portfolio and to the performance recorded by the Bernin I plant (200mm wafers) which has been running at full capacity and benefited from greater productivity, hence from higher volumes, but also from a good control over the production costs. In the meantime, the level of capacity utilization at the Bernin II facility (300mm wafers) remained low, at 19% on average in FY’17.

The overall manufacturing margin[1] reached 31% of wafer sales in H1’17 and 35% of wafer sales in H2’17, improving for the 5th and 6th semester in a row.

Net R&D expenses rose to 18.7 million Euros or 7.6% of revenues, up from 16.7 million Euros or 7.1% of revenues in FY’16. This is essentially due to an increase in gross R&D expenses which amounted to 45.2 million Euros, reflecting Soitec’s commitment to continue investing in the future. A small decline in prototype sales was offset by an increase of a similar amount in subsidies and income tax credit.

Sales and marketing expenses went up to 7.8 million Euros from 5.6 million Euros in FY’16, reflecting preparation for future growth. In the meantime, general and administrative expenses were up to 23.2 million Euros from 17.7 million Euros in FY’16. All in all, FY’17 selling, general and administrative expenses came to 31.0 million Euros or 12.6% of revenues, compared with 10.0% in the previous financial year. This is essentially reflecting an increase in total payroll.

FY’17 current operating income came to 27.7 million Euros, up by 24% compared with a current operating income of 22.4 million Euros in the previous financial year.

In FY’17, the EBITDA4 of the continuing operations (Electronics) stands at 41.0 million Euros, or 16.7% of sales, in line with the latest target of a minimum level of 16.5%. This compares with an EBITDA1 of 36.3 million Euros, or 15.6% of sales in FY’16.

Net result in positive territory

Group consolidated income statement (part 2)

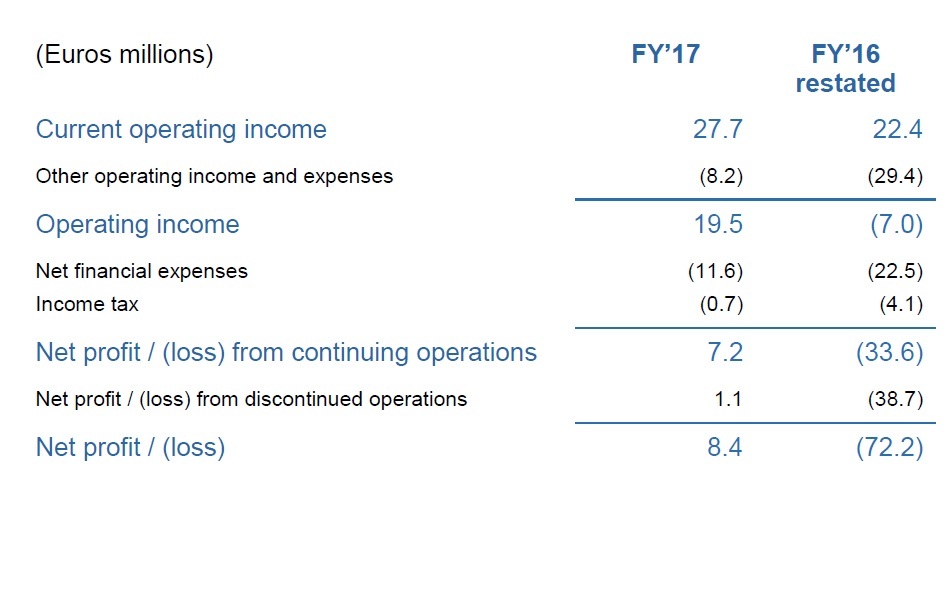

A net amount of 8.2 million Euros was recognized in other operating expenses as a result of an industrial property litigation with Silicon Genesis Corporation (SiGen) in the United States. At the end of March 2017, both companies have agreed to dismiss all pending litigations. This compares with a net amount of 29.4 million Euros recognized in other operating expenses in FY’16, mainly as a result of an impairment loss of 20.1 million Euros on non-current assets (industrial building in Singapore).

The operating income totaled 19.5 million Euros, compared with an operating loss of 7.0 million Euros in the previous financial year.

The Group recorded net financial expenses of 11.6 million Euros, compared with a charge of 22.5 million Euros in the previous financial year.

Interest expense related to the OCEANE bonds went down from 10.2 million Euros to 4.7 million Euros following the repayment of close to 60% of these bonds in June 2016, but a one-off additional charge of 2.2 million Euros related to this repurchase was recorded. Interest expense on the bridging loans granted by CEA, Shin Etsu Handotai and BPIfrance went down from 3.3 million Euros to 0.4 million Euros as a result of the full repayment in May 2016 of these loans. Interest expense on finance leases went slightly down from 1.3 to 1.1 million Euros. Depreciation of financial assets amounted to 0.6 million Euros versus 0.4 million Euros in FY’16. In relation with the security deposit on the Touwsrivier Solar Power Plant bond in South Africa, a financial income of 1.2 million Euros was recognized whilst a provision of 5.0 million Euros was made in FY’16. Finally, a net foreign exchange loss of 2.5 million Euros was recorded in FY’17 compared to a net loss of 1.1 million Euros in FY’16.

Income tax was limited to 0.7 million Euros compared to 4.1 million Euros in FY’16 (there was a one-off charge in the US in FY’16).

Net profit after tax from continuing operations therefore stood at 7.2 million Euros in FY’17 compared with a net loss of 33.6 million Euros in FY’16.

Following the withdrawal from the Solar activities as well as from the Lighting and Equipment activities, the residual income and expenses related to these businesses are recorded under discontinued operations. With an operating loss of 4.8 million Euros (versus 10.9 million Euros in FY’16) and a net financial income of 6.8 million Euros (versus a loss of 27.1 million Euros in FY’16), the net profit from discontinued operations stood at 1.1 million Euros compared to a net loss of 38.7 million Euros in FY’16.

As a result, Soitec recorded a net profit of 8.4 million Euros in FY’17, compared with a net loss of 72.2 million Euros in the previous financial year.

Net cash generation boosted by operating and financing activities

FY’17 cash-flow statement

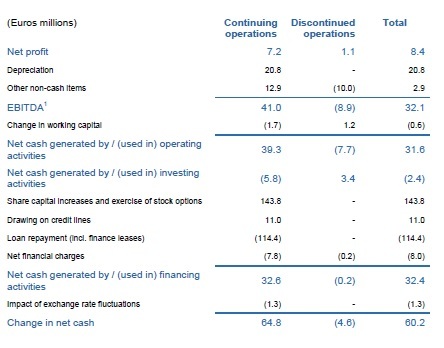

In FY’17, net cash generated by operating activities reached 31.6 million Euros. This came from an inflow of 39.3 million Euros generated by the continuing operations, mitigated by an outflow of 7.7 million euros used by the discontinued activities.

Non-cash items related to the continuing operations amount to 33.8 million Euros, including 20.8 million Euros of depreciation. The EBITDA1 of the continuing operations (Electronics) stands at 41.0 million Euros (up 13% compared to FY’16) whilst the change in working capital was slightly negative by 1.7 million Euros.

A net amount of cash of 5.8 million Euros was used in investing activities related to the continuing operations, whilst financial assets related to the discontinued operations generated 3.4 million Euros. Overall, the net cash used by investing activities amounts to 2.4 million Euros.

Net cash generated by financing activities essentially reflect the strengthening of the balance sheet which was conducted in May and June 2016. Net proceeds from share capital increases amounted to 143.8 million Euros. These proceeds were used to repurchase OCEANE bonds for 58.4 million Euros and to repay expiring bridging loans for around 44.8 million Euros. In addition, Soitec drew 11.0 million Euros on credit lines and paid 8.0 million in net financial charges leading to 32.4 million Euros of net cash generated by financing activities.

Overall, Soitec’s net cash position has increased by a strong 60.2 million Euros during FY’17, thanks in particular to the 39.3 million Euros generated by operating activities of the continuing operations and to the result of the financing activities (essentially capital increases minus bonds and loan repayments) whilst the total cash used by the discontinued operations was limited to 4.6 million Euros.

Major strengthening of Soitec’s financial position

Soitec raised a gross amount of 151.9 million Euros in funds in FY’17 to reinforce its balance sheet and give the Group the financial resources it needs to finance its growth investments. This capital injection was also a mean to strengthen its shareholder structure with Bpifrance, CEA Investissement, and NSIG Sunrise now each holding a 14.5% shareholding in Soitec.

A total of 76.5 million Euros was raised through three increases in capital reserved for Bpifrance Participations, CEA Investissement and NSIG Sunrise, followed by a rights issue through which Soitec raised a gross amount of 75.4 million Euros, including the issue premium. As a result, Soitec shareholders’ equity has been restored, standing at 149.1 million Euros on March 31st, 2017 from negative 7.8 million Euros on March 31st, 2016.

Gross debt was reduced by 98.0 million Euros during the period (from 218.9 to 120.9 million Euros). Indeed, using the funds raised plus a portion of its available cash, Soitec was able to fully redeem its borrowings maturing in May 2016 (around 50 million Euros, including a portion redeemed through the offset of receivables) and buy back a significant part of its 2018 OCEANE bonds (around 60 million Euros out of the total initial issuance of 103 million Euros).

With the funds raised, Soitec has also secured the resources it needs to fund investments in production capacity to manufacture FD-SOI at the Bernin II site (around 40 million Euros). Cash and cash equivalents stand at 109.3 million Euros on March 31st, 2017 compared to 49.1 million Euros on March 31st, 2016.

Net debt consequently stands at 11.6 million Euros on March 31st, 2017 compared to 169.9 million Euros on March 31st, 2016.

Business trends

Demand remains robust for RF-SOI products driven by the growing adoption of LTE Advanced standard in the new generation of smartphones. It is expected that the Front-End module content in smartphones including Antenna Switches, Tuners and new type of devices – LNA (Low Noise Amplifier), will continue to grow demand for RF-SOI in the coming years as this RF-SOI technology today is a standard for these products.

Volumes for Power-SOI keep on experiencing steady growth driven by automotive and “white goods” applications.

Consequently, Bernin I 200mm wafer production site is expected to continue to run at full capacity during FY’18.

As Soitec’s Shanghai-based industrial partner Simgui successfully achieved first customer qualifications for 200mm SOI wafers in October 2016, production has just started in the later part of FY’17 leading to the sale of the very first few thousands 200mm wafers. Industrial production is now expected to ramp up to meet customers’ demand and continue to benefit from sustained growth in 200mm wafers.

In 300mm, a low-point was reached in Q2’17 with a capacity utilization down to 14% as a result of the expected contraction of the activity for PD-SOI products. Production however has started to pick up again in H2’17: the capacity utilization rate reached 29% in Q4’17 and is expected to gradually reach around 50% towards the end of FY’18 / early FY’19.

Indeed, Soitec has benefitted from a significant rise in the sale of other 300mm products, i.e. FD-SOI, RF 300mm and new Emerging SOI products, including platforms that are key for silicon photonics component integration used for data centers and platforms that bring major advantages for image sensors.

In the meantime, the FD-SOI ecosystem continues to strengthen: further progress in the adoption of FD-SOI by the semi-conductor industry was achieved in the past few months.

FD-SOI customers have confirmed their engagement with new factories plans (e.g. GlobalFoundries plant at Chengdu, China) and with new features such as embedded memory and new nodes to further expand their offer (12FDX for GlobalFoundries and 18nmFDS for Samsung). The list of end products benefitting from FD-SOI technology is expanding from the first FD-SOI consumer products: Sony’s GPS embedded in Huami Amazfit Smartwatch and Casio Pro Trek Smartwatch, Mobileye’s EyeQ4 and DreamChip solution for automotive driver assistance, NXP’s i.MX series (7ULP, 8) for consumer applications (like Amazon Alexa) are main examples of FD-SOI adoptions. FD-SOI based products will more and more be present in our daily’s electronics with a growth that will gain momentum with further FD-SOI opportunities coming from IOT and Mobile 5G transceivers.

Still in 300mm, multiple foundries and their fabless customers are engaged in the development of products based on 300mm wafers for RF and volume ramp up is expected in FY’18.

Finally, Soitec is confident in its capacity to build on the recent success of its Photonics-SOI and Imager-SOI products.

Capex plan

Regarding its capex plan, Soitec has made the decision to go ahead with the 40 million Euros investment at Bernin II aimed at progressively increase FD-SOI production capacity from 100,000 to 400,000 FD-SOI wafers (300mm) per year whilst Bernin II full capacity will remain at 650,000 wafers per year. These capex will be spread between FY’18 and FY’19. The process has actually started and the first part of these capex has already been incurred.

In order to address long-term demand for FD-SOI wafers, Soitec intends to reopen its 300mm facility in Singapore. Net cost related to the restarting of the plant would amount to approximately 20 million Euros, to be spread over a period of 24 months once the decision to reopen Singapore is made. The total contemplated investment would reach approximately 270 million US Dollars to bring the production capacity up to 800,000 wafers per year (300mm), including a qualification line worth 40 million US Dollars of which investment will be spent over a period of 24 months following the decision to reopen Singapore. Customer commitments would trigger the gradual roll out of the capex plan. All financing options are currently being considered, with the final choice likely to be determined by the timing of the investment.

FY’18 outlook

FY’18 sales are expected to grow by around 25% at constant exchange rates. Sustained demand is expected in RF-SOI (200mm) and Power-SOI (200mm) leading Bernin I production site to continue operating at full capacity whilst Soitec will also marginally benefit from Simgui capacity. In the meantime, Soitec’s 300mm business is expected to keep on recovering in FY’18 from the low point reached in Q2’17 with further growth coming in all three families (RF-SOI, FD-SOI, Emerging SOI) more than offsetting lower sales of PD-SOI products.

FY’18 Electronics EBITDA1 margin2 is expected to reach a minimum of 20%. Operating profitability will further benefit from the high manufacturing margin of Bernin I production site which, as indicated, is expected to continue operating at full capacity. The strong increase foreseen in the Soitec’s FY’18 Electronics EBITDA1 margin2 will however mainly come from the higher operating leverage of Bernin II production site, as result of a higher utilization rate.

Disclaimer

This document was prepared by Soitec (the “Company”) on June 14, 2017 in connection with the announcement of the fiscal year end 2017 results.

This document is provided for information purposes only. It is public information only.

The Company’s business operations and financial position is described in the Company’s Document de Référence 2016-2017 registered by the Autorité des marchés financiers (the “AMF”) (the “Document de Référence”). Copies of the French language Document de Référence are available through the Company and may also be consulted on the AMF’s website (www.amf-france.org) and on the Company’s website (www.soitec.com).

Your attention is drawn to the risk factors described in Chapter 4 of the Document de Référence. This document contains summary information and should be read in conjunction with the Document de Référence. In the event of a discrepancy between this document and the Document de Référence, the Document de Référence shall prevail.

The information contained in this document has not been independently verified. No representation, warranty or undertaking, express or implied, is made as to, and you may not rely on, the fairness, accuracy, completeness or correctness of the information and opinions contained in this document. The information contained in this document is provided only as of the date hereof. Neither the Company, nor its shareholders or any of their respective subsidiaries, advisors or representatives, accept any responsibility or liability whatsoever for any loss arising from the use of this document or its contents or in connection whatsoever with this document.

This document contains certain forward-looking statements. These forward-looking statements relate to the Company’s future prospects, developments and strategy and are based on analyses of earnings forecasts and estimates of amounts not yet determinable. By their nature, forward-looking statements are subject to a variety of risks and uncertainties as they relate to future events and are dependent on circumstances that may or may not materialize in the future. Forward-looking statements are not a guarantee of the Company’s future performance. The Company’s actual financial position, results and cash flows, as well as the trends in the sector in which the Company operates may differ materially from those contained in this document. Furthermore, even if the Company’s financial position, results, cash-flows and the developments in the sector in which the Company operates were to conform to the forward-looking statements contained in this document, such elements cannot be construed as a reliable indication of the Company’s future results or developments. The Company does not undertake any obligation to update or make any correction to any forward-looking statement in order to reflect an event or circumstance that may occur after the date of this document. In addition, the occurrence of any of the risks described in Chapter 4 of the Document de Référence may have an impact on these forward-looking statements.

This document does not constitute or form part of an offer or a solicitation to purchase or subscribe for the Company’s securities in any country whatsoever. This document, or any part thereof, shall not form the basis of, or be relied upon in connection with, any contract, commitment or investment decision.

Notably, this document does not constitute an offer or solicitation to purchase securities in the United States. Securities may not be offered or sold in the United States absent registration or an exemption from the registration under the U.S. Securities Act of 1933, as amended (the “Securities Act”). The Company’s shares have not been and will not be registered under the Securities Act. Neither the Company nor any other person intends to conduct a public offering of the Company’s securities in the United States.

Agenda

Q1’18 sales is due to be published on July 19th, 2017 after market close.

About Soitec

Soitec (Euronext, Tech 40 Paris) is a world leader in designing and manufacturing innovative semiconductor materials. The company uses its unique technologies and semiconductor expertise to serve the electronics markets. With more than 3,000 patents worldwide, Soitec’s strategy is based on disruptive innovation to answer its customers’ needs for high performance, energy efficiency and cost competitiveness. Soitec has manufacturing facilities, R&D centers and offices in Europe, the U.S. and Asia.

Follow us on Twitter: @Soitec_EN

[1] The EBITDA represents the operating gain (EBIT) before depreciation, amortization, non-monetary items related to share-based payments, and changes in provisions on current assets and provisions for risks and contingencies. This indicator is a non-IFRS quantitative measure used to measure the company’s ability to generate cash from its operating activities. EBITDA is not defined by an IFRS standard and must not be considered an alternative to any other financial indicator.

[2] Electronics EBITDA margin = EBITDA from continuing operations / Sales.

[3] The audit procedures on the consolidated accounts have been performed. Auditors works for documentation are currently being finalized. The certification report will be issued after completion of the last verifications of the management report and the annex to the financial statements.

[4] The manufacturing margin represents the wafer sales (total sales excluding royalties and IP revenues) less cost of sales before distribution costs, before costs related to sales of royalties and costs of patent rights (essentially paid to CEA-Leti in connection with the use of the Smart Cut™ technology). Cost of sales represent the production costs (including the cost of raw materials, essentially silicon), the manufacturing costs (including direct staff cost), the depreciation charges as well as maintenance costs related to production equipment and clean room facilities, and the share of general expense allocated to production. Sales and costs related to Simgui are included in the manufacturing margin. Manufacturing margin is not defined by an IFRS standard and must not be considered an alternative to any other financial indicator.